数据与计算发展前沿 ›› 2023, Vol. 5 ›› Issue (4): 139-153.

CSTR: 32002.14.jfdc.CN10-1649/TP.2023.04.012

doi: 10.11871/jfdc.issn.2096-742X.2023.04.012

• 技术与应用 • 上一篇

田一擎1( ),程曦2,冯博靖2,*()

),程曦2,冯博靖2,*()

收稿日期:2022-04-26

出版日期:2023-08-20

发布日期:2023-08-23

通讯作者:

*冯博靖(E-mail: 作者简介:田一擎,湖南大学,工商管理学院,本科生,主要研究会计学和财务管理。基金资助:

TIAN Yiqing1(),CHENG Xi2,FENG Bojing2,*()

Received:2022-04-26

Online:2023-08-20

Published:2023-08-23

摘要:

【目的】企业信用评级是社会经济有序和健康发展的客观要求和必然选择,本文旨在全面介绍人工智能和大数据时代企业信用评级的主要方法。【方法】通过对国内外的相关文献进行阅读和研究,本文对企业信用评级进行了系统的综述。本文从统计模型、机器学习模型和神经网络模型3个层面梳理了企业信用评级方法发展的脉络,总结了企业信用评级常用数据库,并且深入对比了主要模型的优缺点。最后本文提出了企业信用评级研究中存在的问题,对企业信用评级方法进行了总结与展望。【结果】本文为学术界和企业界了解企业信用评级的量化建模和数据资源提供了系统深入的导引。【结论】神经网络模型在企业信用评级领域仍然存在诸多瓶颈问题,动态图神经网络融合了神经网络的强大表达能力和图结构数据的可解释能力,并引入了时序信息,在企业信用评级领域有广阔的应用前景。

田一擎, 程曦, 冯博靖. 企业信用评级计算模型综述[J]. 数据与计算发展前沿, 2023, 5(4): 139-153.

TIAN Yiqing, CHENG Xi, FENG Bojing. A Review of Computational Models for Corporate Credit Rating[J]. Frontiers of Data and Computing, 2023, 5(4): 139-153, https://cstr.cn/32002.14.jfdc.CN10-1649/TP.2023.04.012.

表1

企业信用评级常用数据库"

| 数据库 | 简介 |

|---|---|

| RESSET | 中国的一个综合性数据平台,提供全世界金融市场相关数据;主要包括股票、黄金、研究报告、宏观统计等系列 |

| 上市公司财务报告 | 上市公司对企业生产经营概况、财务状况等信息进行披露的报告 |

| 中国人民银行征信系统 | 中国国内最全的企业和个人征信数据库 |

| CSMAR | 针对中国国情开发的经济金融领域的研究型精准数据库,2001年创建;涵盖因子研究、绿色经济、股票、资讯、基金等18大系列,包含160多个数据库、4,000多张表、5万多个字段 |

| WRDS | 由宾夕法尼亚大学沃顿商学院于1993年开发的金融领域的跨库研究工具,整合了Compustat、CRSP、TFN、TAQ等多个著名数据库 |

| Bloomberg | 全球最大的财经资讯、金融数据服务提供商 |

| FAME | 覆盖了英国和爱尔兰的380万家公司的信息 |

| UCI机器学习知识库 | 加州大学欧文分校提出的用于机器学习的数据库 |

| Compustat | 标准普尔发布的数据库,收录北美及全球上市公司近20年的财务数据 |

| CRSP | 由芝加哥大学商学研究生院成立,是证券领域极具权威的数据库,广泛收录了美国上市公司的股票价格和交易数据 |

| 日经NEEDS | 日本最大的综合经济数据库,涵盖了从宏观经济到企业财务多个层面 |

| Bankscope | BureauvanDijk与银行业权威评级机构惠誉公司合作开发的银行业信息库;提供了全球12,800多家主要银行及世界重要金融机构与组织的经营与信用分析数据 |

| WIND | 由中国企业万得资讯提供,是以金融证券财经数据为核心的数据库 |

| KIS-VALUE | 韩国一个提供企业报务报表及股市数据分析的数据库 |

表2

企业信用评级常用指标"

| 类别 | 指标 |

|---|---|

| 规模 | 总资产 |

| 总资本 | |

| 总现金流 | |

| 权益总额 | |

| 资本支出总额 | |

| 市值 | |

| 总交易量 | |

| 债务总额 | |

| 盈利能力 | 息税前收益 |

| 税后收入 | |

| 净利润增长 | |

| 净资产销售额 | |

| 总资产销售额 | |

| 非现金营运资本 | |

| 上一年的销售 | |

| 股市 | 红利 |

| 每股收益的增长 | |

| 市盈率 | |

| 留存收益 | |

| 股价 | |

| 已发行股份数量 |

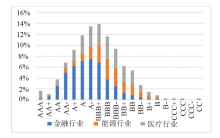

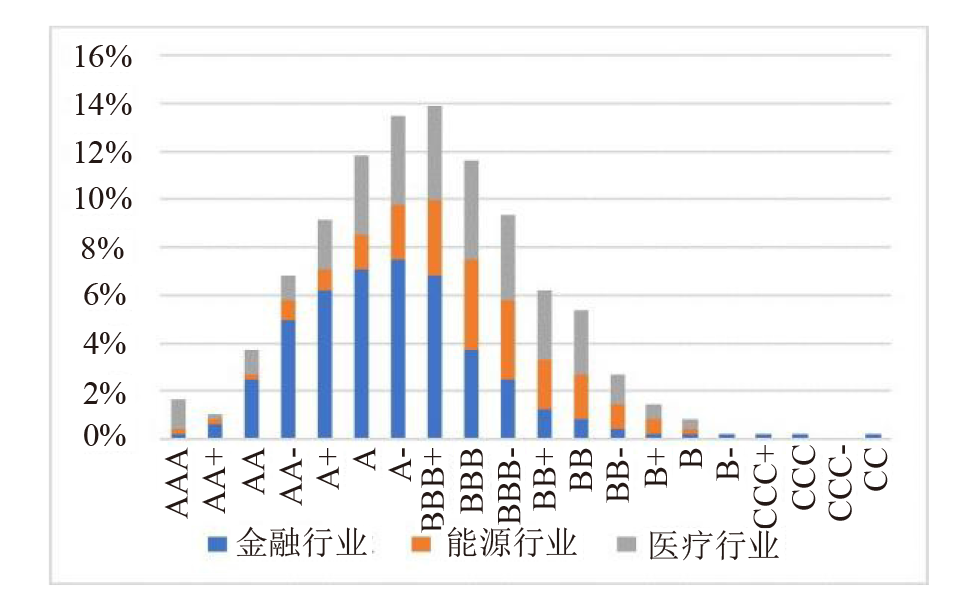

图 1

典型行业的企业信用评级分布图"

| [1] |

Hajek P, Michalak K. Feature selection in corporate credit rating prediction[J]. Knowledge-Based Systems, 2013, 51: 72-84.

doi: 10.1016/j.knosys.2013.07.008 |

| [2] |

Kim K, Ahn H. A corporate credit rating model using multi-class support vector machines with an ordinal pairwise partitioning approach[J]. Computers & Operations Research, 2012, 39(8): 1800-1811.

doi: 10.1016/j.cor.2011.06.023 |

| [3] |

Huang Z, Chen H, Hsu C J, et al. Credit rating analysis with support vector machines and neural networks: a market comparative study[J]. Decision support systems, 2004, 37(4): 543-558.

doi: 10.1016/S0167-9236(03)00086-1 |

| [4] |

Altman E I, Haldeman R G, Narayanan P. ZETATM analysis A new model to identify bankruptcy risk of corporations[J]. Journal of banking & finance, 1977, 1(1): 29-54.

doi: 10.1016/0378-4266(77)90017-6 |

| [5] |

Yurdakul M, Ic Y T. Development of a performance measurement model for manufacturing companies using the AHP and TOPSIS approaches[J]. International Journal of Production Research, 2005, 43(21): 4609-4641.

doi: 10.1080/00207540500161746 |

| [6] | Gu W, Basu M, Chao Z, et al. A unified framework for credit evaluation for internet finance companies: Multi-criteria analysis through AHP and DEA[J]. International Journal of Information Technology & Decision Making, 2017, 16(3): 597-624. |

| [7] | Yang S, Islam M T. Principal Component Analysis and Factor Analysis for Feature Selection in Credit Rating[EB/OL].[2020-12-21]. https://arxiv.org/abs/2011.09137. |

| [8] | Reichert A K, Cho C C, Wagner G M. An examination of the conceptual issues involved in developing credit-scoring models[J]. Journal of Business & Economic Statistics, 1983, 1(2): 101-114. |

| [9] |

Altman E I, Saunders A. Credit risk measurement: Developments over the last 20 years[J]. Journal of banking & finance, 1997, 21(11-12): 1721-1742.

doi: 10.1016/S0378-4266(97)00036-8 |

| [10] | Friedman J H. Multivariate adaptive regression splines[J]. The annals of statistics, 1991, 19(1): 1-67. |

| [11] |

Laitinen E K. Predicting a corporate credit analyst’s risk estimate by logistic and linear models[J]. International review of financial analysis, 1999, 8(2): 97-121.

doi: 10.1016/S1057-5219(99)00012-5 |

| [12] |

West R C. A factor-analytic approach to bank condition[J]. Journal of Banking & Finance, 1985, 9(2): 253-266.

doi: 10.1016/0378-4266(85)90021-4 |

| [13] | Liang X, Chen S, Liu Y. The study of small enterprises credit evaluation based on incremental AntClust[C]. 2007 IEEE International Conference on Grey Systems and Intelligent Services, IEEE, 2007: 294-298. |

| [14] | Shi B, Meng B, Yang H, et al. A novel approach for reducing attributes and its application to small enterprise financing ability evaluation[J]. Complexity, 2018, 2018: 1-17. |

| [15] |

Ic Y T, Yurdakul M. Development of a quick credibility scoring decision support system using fuzzy TOPSIS[J]. Expert Systems with Applications, 2010, 37(1): 567-574.

doi: 10.1016/j.eswa.2009.05.038 |

| [16] |

Wang Y, Wang S, Lai K K. A new fuzzy support vector machine to evaluate credit risk[J]. IEEE Transactions on Fuzzy Systems, 2005, 13(6): 820-831.

doi: 10.1109/TFUZZ.2005.859320 |

| [17] |

Cao L, Guan L K, Jingqing Z. Bond rating using support vector machine[J]. Intelligent Data Analysis, 2006, 10(3): 285-296.

doi: 10.3233/IDA-2006-10307 |

| [18] |

Lee Y C. Application of support vector machines to corporate credit rating prediction[J]. Expert Systems with Applications, 2007, 33(1): 67-74.

doi: 10.1016/j.eswa.2006.04.018 |

| [19] |

Huang C L, Chen M C, Wang C J. Credit scoring with a data mining approach based on support vector machines[J]. Expert systems with applications, 2007, 33(4): 847-856.

doi: 10.1016/j.eswa.2006.07.007 |

| [20] |

Zhu P, Hu Q. Rule extraction from support vector mach-ines based on consistent region covering reduction[J]. Knowledge-Based Systems, 2013, 42: 1-8.

doi: 10.1016/j.knosys.2012.12.003 |

| [21] |

Maldonado S, Pérez J, Bravo C. Cost-based feature selection for support vector machines: An application in credit scoring[J]. European Journal of Operational Research, 2017, 261(2): 656-665.

doi: 10.1016/j.ejor.2017.02.037 |

| [22] | Gu T, Yang S. Duration prediction for truck crashes based on the XGBoost algorithm[M]. CICTP 2019, 2019: 5021-5031. |

| [23] |

Florez-Lopez R, Ramon-Jeronimo J M. Enhancing accuracy and interpretability of ensemble strategies in credit risk assessment. A correlated-adjusted decision forest proposal[J]. Expert Systems with Applications, 2015, 42(13): 5737-5753.

doi: 10.1016/j.eswa.2015.02.042 |

| [24] |

Yeh C C, Lin F, Hsu C Y. A hybrid KMV model, random forests and rough set theory approach for credit rating[J]. Knowledge-Based Systems, 2012, 33: 166-172.

doi: 10.1016/j.knosys.2012.04.004 |

| [25] |

Abellán J, Castellano J G. A comparative study on base classifiers in ensemble methods for credit scoring[J]. Expert systems with applications, 2017, 73: 1-10.

doi: 10.1016/j.eswa.2016.12.020 |

| [26] | Donate J P, Cortez P, Sanchez G G, et al. Time series forecasting using a weighted cross-validation evo-lutionary artificial neural network ensemble[J]. Neuro-computing, 2013, 109: 27-32. |

| [27] |

Yu L, Wang S, Lai K K. Credit risk assessment with a multistage neural network ensemble learning approach[J]. Expert systems with applications, 2008, 34(2): 1434-1444.

doi: 10.1016/j.eswa.2007.01.009 |

| [28] |

He H, Zhang W, Zhang S. A novel ensemble method for credit scoring: Adaption of different imbalance ratios[J]. Expert Systems with Applications, 2018, 98: 105-117.

doi: 10.1016/j.eswa.2018.01.012 |

| [29] | Chornous G, Nikolskyi I. Business-oriented feature selection for hybrid classification model of credit scoring[C]. 2018 IEEE Second International Conference on Data Stream Mining & Processing (DSMP), IEEE, 2018: 397-401. |

| [30] | Wang M, Ku H. Utilizing historical data for corporate credit rating assessment[J]. Expert Systems with Appli-cations, 2021, 165: 113925. |

| [31] |

Chen Y S, Cheng C H. Hybrid models based on rough set classifiers for setting credit rating decision rules in the global banking industry[J]. Knowledge-Based Systems, 2013, 39: 224-239.

doi: 10.1016/j.knosys.2012.11.004 |

| [32] |

Chai N, Wu B, Yang W, et al. A multicriteria approach for modeling small enterprise credit rating: evidence from China[J]. Emerging Markets Finance and Trade, 2019, 55(11): 2523-2543.

doi: 10.1080/1540496X.2019.1577237 |

| [33] |

Chen B, Long S. A novel end-to-end corporate credit rating model based on self-attention mechanism[J]. IEEE Access, 2020, 8: 203876-203889.

doi: 10.1109/Access.6287639 |

| [34] | Golbayani P, Wang D, Florescu I. Application of deep neural networks to assess corporate credit rating[EB/OL]. [2020-3-4]. https://arxiv.org/abs/2003.02334. |

| [35] | Brennan D, Brabazon A. Corporate Bond Rating Using Neural Networks[C]. IC-AI, 2004: 161-167. |

| [36] |

Angelini E, Di Tollo G, Roli A. A neural network approach for credit risk evaluation[J]. The quarterly review of economics and finance, 2008, 48(4): 733-755.

doi: 10.1016/j.qref.2007.04.001 |

| [37] |

Choi J, Suh Y, Jung N. Predicting corporate credit rating based on qualitative information of MD&A transformed using document vectorization techniques[J]. Data Technologies and Applications, 2020, 54(2): 151-168.

doi: 10.1108/DTA-08-2019-0127 |

| [38] | Du Y. Enterprise credit rating based on genetic neural network[C]. MATEC Web of Conferences. EDP Sciences, 2018, 227: 02011. |

| [39] |

Luo C, Wu D, Wu D. A deep learning approach for credit scoring using credit default swaps[J]. Engineering Applications of Artificial Intelligence, 2017, 65: 465-470.

doi: 10.1016/j.engappai.2016.12.002 |

| [40] |

Kim K S. Predicting bond ratings using publicly available information[J]. Expert Systems with Applications, 2005, 29(1): 75-81.

doi: 10.1016/j.eswa.2005.01.007 |

| [41] | Hájek P. Probabilistic Neural Networks for Credit Rating Modelling[C]. IJCCI (ICFC-ICNC), 2010: 289-294. |

| [42] | Fu K, Cheng D, Tu Y, et al. Credit card fraud detection using convolutional neural networks[C]. International conference on neural information processing, Springer, Cham, 2016: 483-490. |

| [43] | Rajaa S, Sahoo J K. Convolutional feature extraction and neural arithmetic logic units for stock prediction[C]. International Conference on Advances in Computing and Data Sciences, Springer, Singapore, 2019: 349-359. |

| [44] |

Dixon M, Klabjan D, Bang J H. Classificationbased fin-ancial markets prediction using deep neural networks[J]. Algorithmic Finance, 2017, 6(3-4): 67-77.

doi: 10.3233/AF-170176 |

| [45] | Feng B, Xue W, Xue B, et al. Every corporation owns its image: Corporate credit ratings via convolutional neural networks[C]. 2020 IEEE 6th International Conference on Computer and Communications (ICCC), IEEE, 2020: 1578-1583. |

| [46] | Mikolov T, Chen K, Corrado G, et al. Efficient estimation of word representations in vector space[EB/OL]. [2014-9-7]. https://arxiv.org/abs/1301.3781. |

| [47] | Le Q, Mikolov T. Distributed representations of sentences and documents[C]. International conference on machine learning, PMLR, 2014: 1188-1196. |

| [48] | Feng B, Xu H, Xue W, et al. Every corporation owns its structure: Corporate credit ratings via graph neural networks[EB/OL]. [2020-11-27]. https://arxiv.org/abs/2012.01933. |

| [49] | Feng B, Xue W. Adversarial semi-supervised learning for corporate credit ratings[J]. The Journal of Software, 2021, 16(6): 259-266. |

| [50] | Feng B, Xue W. Contrastive Pre-training for Imbalanced Corporate Credit Ratings[EB/OL]. [2022-2-23]. https://arxiv.org/abs/2102.12580. |

| [51] | Plumb G, Molitor D, Talwalkar A S. Model agnostic supervised local explanations[J]. Advances in neural information processing systems, 2018, 31: 1-10. |

| [52] | Wang D, Chen Z, Florescu I. A Sparsity Algorithm with Applications to Corporate Credit Rating[EB/OL]. [2021-7-21]. https://arxiv.org/abs/2107.10306. |

| [1] | 孟哲, 余粟. 基于Spark和优化BP神经网络的出租车需求预测模型[J]. 数据与计算发展前沿, 2023, 5(4): 112-126. |

| [2] | 陈美霖, 刘端阳, 徐黎明, 汪洋. 基于机器学习的力场模型研究综述[J]. 数据与计算发展前沿, 2023, 5(4): 27-37. |

| [3] | 刘端阳, 魏钟鸣. 有监督学习算法在材料科学中的应用[J]. 数据与计算发展前沿, 2023, 5(4): 38-47. |

| [4] | 陈栋, 李明, 陈淑文. 结合Transformer和多层特征聚合的高光谱图像分类算法[J]. 数据与计算发展前沿, 2023, 5(3): 138-151. |

| [5] | 李妍,何洪波,王闰强. 微博热度预测研究综述[J]. 数据与计算发展前沿, 2023, 5(2): 119-135. |

| [6] | 高添,朱教君,张金鑫,孙一荣,于丰源,滕德雄,卢德亮,于立忠,王宗国. 基于新一代信息技术的温带森林生态系统碳通量精准计量[J]. 数据与计算发展前沿, 2023, 5(2): 60-72. |

| [7] | 王凡,冯立强,曹荣强. 大数据驱动的海洋人工智能服务平台设计与应用[J]. 数据与计算发展前沿, 2023, 5(2): 73-85. |

| [8] | 许淞源,刘峰. ESDRec:一种面向地球大数据平台的数据推荐模型[J]. 数据与计算发展前沿, 2023, 5(1): 55-64. |

| [9] | 童昭,王露笛,朱小杰,杜一. 基于预训练模型的军事领域命名实体识别研究[J]. 数据与计算发展前沿, 2022, 4(5): 120-128. |

| [10] | 赵忠斌,蔡满春,芦天亮. 融合多头注意力机制的网络恶意流量检测[J]. 数据与计算发展前沿, 2022, 4(5): 60-67. |

| [11] | 石雪梅,朱克亮,张祥民,张树涛,陈良锋. 基于生成对抗网络的有遮挡人脸修复方法[J]. 数据与计算发展前沿, 2022, 4(4): 123-131. |

| [12] | 危婷,张宏海,蔺小丽,张蕾蕾,王妍,贾金峰. 云服务网站用户复访行为预测模型研究[J]. 数据与计算发展前沿, 2022, 4(3): 124-130. |

| [13] | 孙永谦,张茹茹,林子涵,张圣林,谭智元,张玉志. KPI异常检测方法评估[J]. 数据与计算发展前沿, 2022, 4(3): 46-65. |

| [14] | 肖楠,周明珠,邢军,罗泽,李晓辉. 基于高分辨率网络和注意力机制的真伪卷烟包装鉴别[J]. 数据与计算发展前沿, 2021, 3(5): 118-129. |

| [15] | 张猛,李健. 鸟类音频数据预处理方法[J]. 数据与计算发展前沿, 2021, 3(5): 130-140. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||