Frontiers of Data and Computing ›› 2024, Vol. 6 ›› Issue (6): 146-159.

CSTR: 32002.14.jfdc.CN10-1649/TP.2024.06.014

doi: 10.11871/jfdc.issn.2096-742X.2024.06.014

ZHANG Bin1,2( ),LI Chen1,LU Zhonghua1,*()

),LI Chen1,LU Zhonghua1,*()

Received:2023-12-26

Online:2024-12-20

Published:2024-12-20

Contact:

LU Zhonghua

E-mail:bzhang98@zzu.edu.cn;zhlu@cnic.cn

ZHANG Bin,LI Chen,LU Zhonghua. A Survey of Research on Risk Factors in the Chinese Stock Market[J]. Frontiers of Data and Computing, 2024, 6(6): 146-159, https://cstr.cn/32002.14.jfdc.CN10-1649/TP.2024.06.014.

Table 1

Factor models"

| 模型 | 增加因子 |

|---|---|

| CAPM | 市场因子 |

| 三因子模型 | 市值因子、账面市值比 |

| 多因子模型 | 投资因子、盈利能力因子、情绪因子、波动率因子等 |

Table 2

Comparison of risk factors between manual and machine construction"

| 人工 | 机器学习 | |

|---|---|---|

| 数据类型 | 大部分只可拟合线性数据 | 可拟合线性和非线性数据 |

| 数据量 | 较少 | 较多 |

| 可解释性 | 较强 | 较差 |

| 算力要求 | 较低 | 较高 |

| 适用范围 | 较广 | 大多数只应用于大盘或个股 |

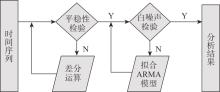

Fig.1

ARIMA flowchart"

Table 3

Information about constructing risk factor b-ased on RNN and CNN"

| 文献 | 因子类型 | 数据 | 模型 |

|---|---|---|---|

| [ | 预测涨跌 | 开盘价、收盘价、高价、低价、成交量 | CNN |

| [ | 预测价格 | RNN-CNN | |

| [ | 预测价格 | RNN-MRF | |

| [ | 预测涨跌 | 最高价 | CNN-SVM |

| [ | 预测价格 | 技术特征、内容特征 | RNN-Boost |

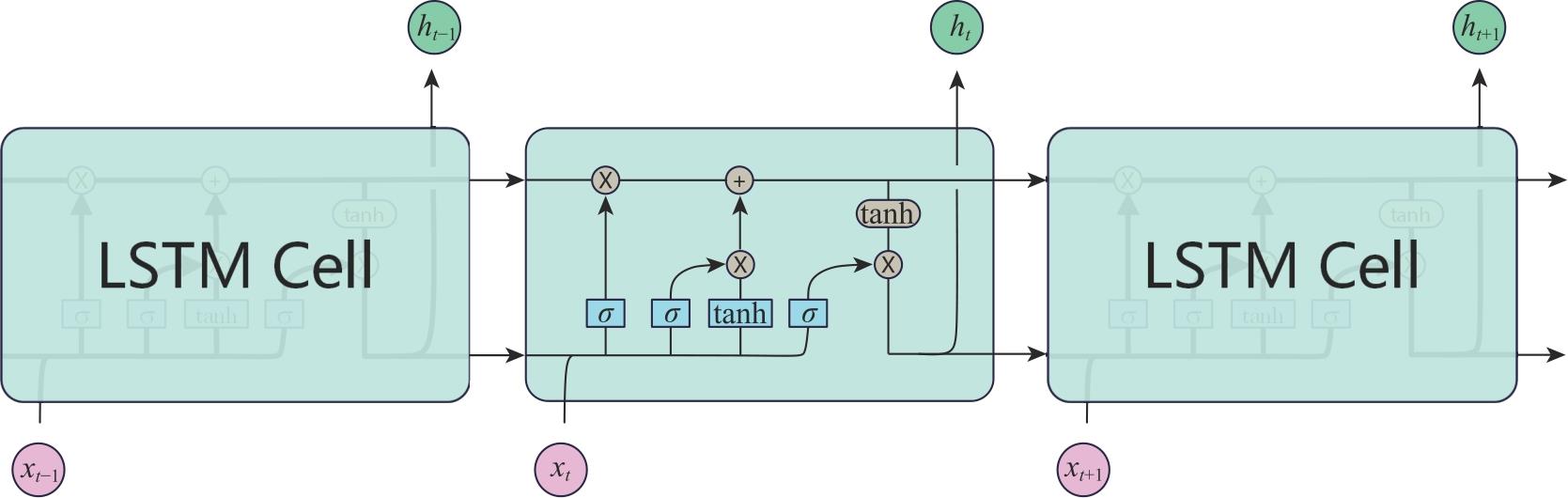

Fig.2

LSTM structure diagram"

Table 4

Information about constructing risk factor based on LSTM"

| 文献 | 因子类型 | 数据 | 模型 |

|---|---|---|---|

| [ | 预测收益 | 收盘价、成交量 | LSTM |

| [ | 预测价格 | 收盘价 | Kmeans-LSTM |

| [ | 预测价格 | 日振幅、成交量波动等 | LSTM |

| [ | 预测价格 | 开盘价、收盘价、成交量和情绪数据 | LSTM |

| [ | 预测涨跌 | 情绪数据 | LSTM |

| [ | 预测价格 | 新闻数据、交易数据 | LSTM-Attention |

| [ | 预测价格 | 收盘价、成交量和EMA等特征指标 | LSTM-WD |

| [ | 预测价格 | 开盘价 | LSTM-MI |

| [ | 预测收益 | 开盘价、收盘价、高价等11个指标 | LSTM |

| [ | 预测买卖 | 开盘价、收盘价、ARIMA输出等 | ARIMA-LSTM |

| [ | 预测价格 | 5分钟高频数据 | ARIMA-LSTM |

| [ | 预测价格 | 交易信息和市场信息 | BiLSTM |

| [ | 预测价格 | 最高价、最低价、利率、汇率等 | LSTM-GA |

| [ | 预测涨跌 | 构建14个特征 | LSTM-CNN |

| [ | 预测价格 | 开盘价、收盘价、高价、低价、成交量、换手率 | LSTM-GCN |

| [ | 预测波动率 | 5分钟高频数据 | LSTM |

| [ | 预测波动率 | 5分钟高频数据 | LSTM |

| [ | 预测波动率 | 高频波动率序列、技术指标、时间序列参数 | LSTM-HIT |

| [ | 预测波动率 | 5分钟高频数据 | RG-RD-LSTM |

| [ | 预测波动率 | 5分钟高频数据、开盘价、收盘价等 | LSTM |

Table 5

Information about constructing risk factors using other models"

| 文献 | 因子类型 | 数据 | 模型 |

|---|---|---|---|

| [ | 预测收益 | 开盘价、高价、低价、收盘价、成交量 | MFNN |

| [ | 预测价格 | 新闻 | HAN |

| [ | 预测价格 | 开盘价、收盘价、高价、低价、 | DRL |

| [ | 预测价格 | 价格信息、异同移动平均线、随机指标 | Stockformer |

| [ | 预测收益 | 5分钟高频数据 | XGBoost |

| [ | 预测涨跌 | 5分钟高频数据和技术指标 | SVM |

| [ | 预测波动率 | 5分钟高频数据 | EEMD-XGBoost |

| [ | 预测价格 | 每5分钟、1小时高频数据 | CEEMDAN_lineformer |

| [ | 预测波动率 | 50ETF基金高频交易数据集 | Transformer |

| [ | 预测价格 | 新闻 | SPMPN |

Table 6

Analysis of the advantages and disadvantages of different models"

| 模型类型 | 优点 | 缺点 |

|---|---|---|

| CNN | 共享卷积核,可以减少参数数量有效的处理高维数据;可以有效的识别到局部数据中的潜在风险 | 容易忽略局部和整体的关系,导致潜在的风险信息被忽略 |

| RNN | 可以挖掘时序数据不同时间数据之间的关系;可以捕捉数据之间的依赖关系从而挖掘风险信息 | 由于计算过程是顺序的,在处理长序列信息时效率较低;难以捕获长期序列数据依赖关系,容易忽略长期时序数据中的风险信息 |

| LSTM | 可以有效的捕获时序数据的长期依赖关系;可以有选择的保留重点风险信息 | 引入的门控机制,使得模型更为复杂,在计算高频时序数据时需要计算的参数量巨大,计算风险因子开销较大 |

| 机器学习混合模型 | 可以结合不同模型的优点,更好的分析特征数据之间的关系,挖掘出更多的潜在风险信息 | 模型通常比较复杂,在分析处理高频数据时效率不高,需要较高的算力支持 |

| 机器学习与传统金融的混合模型 | 可以获得传统金融模型提炼过的信息,从不同的角度获得输入的特征信息 | 通过使用传统金融模型处理过的数据,可能会导致某些关键信息遗漏,从而无法提取到更加全面的潜在风险信息 |

| [1] | KING M, WADHAWANI S. Transmission of Volatility between Stock Markels[J]. Review of Financial Studies, 1990, 3(1): 5-33. |

| [2] | FORBES K, RIGOBON R. No Contagion, Only Intendependence: Measuring Stock Market Comovements[J]. The Journal of Finance, 2002, 57(5): 2223-2261. |

| [3] | KAMINSKY G, REINHART C. On Crises, Contagion, and Confusion[J]. Journal of International Econmics, 2000, 51(1): 145-168. |

| [4] | 王锦涛. 基于LSTM混合模型的金融时间序列预测研究[D]. 郑州大学, 2019. |

| [5] | 王娜, 施建淮. 我国金融稳定指数的构建: 基于主成分分析法[J]. 南方金融, 2017(6): 46-55. |

| [6] | 万校基, 李海林. 基于特征表示的金融多元时间序列数据分析[J]. 统计与决策, 2015(23): 151-155. |

| [7] | SHARPE W. Capital asset prices: A theory of market equilibrium under conditions of risk[J]. Journal of Finance, 1964, 19(3): 425-442. |

| [8] | ROSS S. The arbitrage pricing theory[J]. Journal of Economic Theory, 1976, 13(3): 341-36. |

| [9] | 潘梦梦. 高频视角下中国股票市场系统风险研究[D]. 吉林大学, 2023. |

| [10] | 陈国进, 胥爱欢, 赵向琴. 信息市场、预期消费与资产收益——基于投资者的信息选择行为[J]. 系统工程理论与实践, 2012, 32(3): 597-607. |

| [11] | 温彬, 刘淳, 金洪飞. 宏观经济因素对中国行业股票收益率的影响[J]. 财贸经济, 2011, (6): 51-59. |

| [12] | 马勇, 杨雯葳, 姜伊晴. 投资者情绪如何影响公司股价?[J]. 金融论坛, 2020, 25(5): 57-67. |

| [13] | 宋光辉, 董永琦, 陈杨炀, 等. 中国股票市场流动性与动量效应——基于fama-french五因子模型的进一步研究[J]. 金融经济学研究, 2017, 32(1): 36-50. |

| [14] | 田利辉, 王冠英, 张伟. 三因素模型定价: 中国与美国有何不同?[J]. 国际金融研究, 2014, (7): 37-45. |

| [15] | 孔东民, 林之阳. 企业社会责任、公司价值和基金业绩[J]. 华中科技大学学报(社会科学版), 2017, 32(3): 62-72. |

| [16] | ENGLE R. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation[J]. Econometrica: Journal of the econometric society, 1982, 50(4): 987-1007. |

| [17] | 王立, 佘珍. 基于ARCH族模型的我国CPI波动的实证研究[J]. 经营与管理, 2019(7): 119-123. |

| [18] | 周文龙, 李育冬, 余红心, 等. 投资者情绪与市场收益的双向波动溢出关系——基于TGARCH-M和BEKK-GARCH模型[J]. 金融理论与实践, 2020, (11): 69-78. |

| [19] | 李立林, 施建业. 创业板和沪市主板波动溢出效应研究——基于BEKK-GARCH模型[J]. 北方金融, 2021, (6): 71-75. |

| [20] | 王云, 唐振和, 饶慧君, 等. 美国宽松货币政策对我国金融市场的溢出效应分析——基于S-VAR和DCC-GARCH方法的研究[J]. 华北金融, 2022, (10): 51-58. |

| [21] | BRUNNERMEIER M, GORTON G, KEISHNAMURTHY A. Risk topography[J]. Nber macroeconomics annual, 2012, 26(1): 149-176. |

| [22] | 朱紫薇, 张庆君. 货币政策、企业资本结构与流动性错配——基于房地产业上市公司的数据[J]. 金融理论与实践, 2018(10): 7-15. |

| [23] | 刘精山, 赵沛, 田静. 基于时变模型的商业银行流动性风险度量研究[J]. 财经理论与实践, 2019, 40(6): 16-23. |

| [24] | 郭立仑, 周升起. 商业银行流动性: 风险测度、影响因素和对策研究[J]. 经济学报, 2023, 10(3): 59-83. |

| [25] | ANDERSEN T, BOLLERSLEV T. Answering the skeptics: Yes, standard volatility modelsdo provide accurate forecasts[J]. International Economic Review, 1998, 39(4): 885-905. |

| [26] | CORSI F. A simple approximate long-memory model of realized volatility[J]. Journal of Financial Econometrics, 2009, 7(2): 174-196. |

| [27] | 吴鑫育, 王海运. 基于状态空间HAR-RV- RS模型的中国股市波动率预测[J]. 合肥工业大学学报(社会科学版), 2021, 35(4): 10-19. |

| [28] | BOX G, JENKINS G. Time series analysis: forecasting and control[J]. San Francisco: Holden Bay, 1976, 31(2): 238-242. |

| [29] | 姚金海. 基于ARIMA与信息粒化SVR组合的股指预测研究[J]. 运筹与管理, 2022, 31(5): 214-220. |

| [30] | 姚金海, 邹家骏. CPI预测的SVM-ARIMA模型构建与数值模拟[J]. 统计与决策, 2022, 38(21): 48-52. |

| [31] | 翁紫霞. 基于ARIMA模型的股价分析与预测——以建设银行为例[J]. 现代信息科技, 2023, 7(14): 137-141. |

| [32] | 徐路钧, 赵戊生. 基于ARIMA模型企业自由现金流量的预测[J]. 商业观察, 2023, 9(20): 41-47. |

| [33] | 郭改文, 王诗涵. 基于灰色理论与ARIMA模型的股票价格预测[J]. 河南教育学院学报(自然科学版), 2023, 32(2): 22-27. |

| [34] | ENGLE R, RUSSELL J. Autoregressive conditional duration: a new model for irregualarly spaced transaction data[J]. Econometrica, 1998, 66(5): 1127-1162. |

| [35] | 张欣. 基于高频数据的股票流动性影响因素研究[D]. 南京理工大学, 2017. |

| [36] | BEAVER W. Financial ratios as predictors of failure[J]. Journal of Research, 1966, 4(1): 71-111. |

| [37] | 徐鹏. 基于Logistic-Stacking模型的信用债违约风险预警研究[D]. 浙江财经大学, 2023. |

| [38] | 李鸿禧, 宋宇. 基于时间相依Cox回归的动态财务预警模型及实证[J]. 运筹与管理, 2020, 29(8): 177-185. |

| [39] | 范建华, 张静. 基于Fama-French三因子模型的沪深300指数效应实证研究[J]. 重庆工商大学学报(社会科学版), 2013, 30(3): 31-38. |

| [40] | FAMA E, FRENCH K. A Five-Factor asset pricing model[J]. Journal of Financial Economics, 2015, 116(1): 1-22. |

| [41] | 杜威望, 肖曙光. FF五因子模型在中国股票市场的改进研究[J]. 华侨大学学报(哲学社会科学版), 2018(3): 39-53. |

| [42] | 杜威望. 基于FF五因子模型的基金投资风格分析模型扩展研究[J]. 武汉金融, 2019(10): 52-57. |

| [43] | 刘钰莹. Fama-French三因子模型实证及扩展[D]. 广东外语外贸大学, 2020. |

| [44] | 崔丽芳, 陈喜强. 中国家电行业股票市场的实证研究——基于Fama-French五因子模型分析[J]. 区域金融研究, 2021(1): 49-54. |

| [45] | 朱磊, 刘奇. 我国股票市场超额收益影响因素研究——基于Fama-French五因子模型[J]. 环渤海经济瞭望, 2022(7): 141-143. |

| [46] | 蔡超, 董皓天, 黄聪聪. 基于分位数回归森林+POT的极端VaR风险测度[J]. 山东工商学院学报, 2022, 36(5): 102-108. |

| [47] | 毕克如. 基于POT模型的股票市场风险度量研究[J]. 安阳师范学院学报, 2023(2): 48-52. |

| [48] | 王子仪, 李磊. 金融业与实体经济间系统性风险溢出效应研究——基于GARCH-QRNN-POT模型[J]. 兰州财经大学学报, 2023, 39(2): 76-89. |

| [49] | LECUN Y, BOTTOU L, BENGIO Y, et al. Gradient-based learning applied to document recognition[J]. Proceedings of the IEEE, 1998, 86(11): 2278-2324. |

| [50] | 李文静, 白静, 彭斌, 等. 图卷积神经网络及其在图像识别领域的应用综述[J]. 计算机工程与应用, 2023, 59(22): 15-35. |

| [51] | 张阳婷, 黄德启, 王东伟, 等. 基于深度学习的目标检测算法研究与应用综述[J]. 计算机工程与应用, 2023, 59(18): 1-13. |

| [52] | 赖丽娜, 米瑜, 周龙龙, 等. 生成对抗网络与文本图像生成方法综述[J]. 计算机工程与应用, 2023, 59(19): 21-39. |

| [53] | CHEN S, HE H. Stock prediction using convolutional neural network[C]// IOP Conferenceseries: materials science and engineering. IOP Publishing, 2018, 435: 012026. |

| [54] | CAO J, WANG J. Stock price forecasting model based on modified convolution neural network and financial time series analysis[J]. International Journal of Communication Syst-ems, 2019, 32(12): e3987. |

| [55] | CHEN W, YEO C, LAU C, et al. Leveraging social media news to predict stock index movement using RNN-boost[J]. Data & Kno-wledge Engineering, 2018, 118: 14-24. |

| [56] | ZHANG R, YUAN Z, SHAO X. A new combined CNN-RNN model for sector stock price analysis[C]// 2018 IEEE 42nd Annual Computer Software and Applications Conference (COMPSAC), IEEE, 2018, 2: 546-551. |

| [57] | LI C, SONG D, TAO D. Multi-task recurrent neural networks and higher-order Markov random fields for stock price movement prediction: Multi-task RNN and higer-order MRFsfor stock price classification[C]// Proceedings of the 25th ACM SIGKDD international conference on knowledge discovery & data mining, 2019: 1141-1151. |

| [58] | CHEN K, ZHOU Y, DAI F. A LSTM-based method for stock returns prediction: A case study of China stock market[C]// 2015 IEEE international conference on big data (big data), IEEE, 2015: 2823-2824. |

| [59] | SHAO X, MA D, LIU Y, et al. Short-term forecast of stock price of multi-branch LSTM based on K-means[C]// 2017 4th International Conference on Systems and Informatics (ICSAI), IEEE, 2017: 1546-1551. |

| [60] | ZHAO Z, RAO R, TU S, et al. Time-weighted LSTM model with redefined labeling for stock trend prediction[C]// 2017 IEEE 29thinternational conference on tools with artificial intelligence (ICTAI), IEEE, 2017: 1210-1217. |

| [61] | LI J, BU H, WU J. Sentiment-aware stock market prediction: A deep learning method[C]// 2017 international conference on service systems and service management, IEEE, 2017: 1-6. |

| [62] | CHEN M, LIAO C, HSIEH R. Modeling public mood and emotion: Stock market trend prediction with anticipatory computing approach[J]. Computers in Human Behavior, 2019, 101: 402-408. |

| [63] | 刘怡萱. 基于深度学习融合情感分析和知识图谱的股票趋势预测研究[D]. 杭州电子科技大学, 2023. |

| [64] | LI Z, TAM V.Combining the real-time wavelet denoising and long-short-term-memory neural network for predicting stock indexes[C]// 2017 IEEE Symposium Series on Computational Intelligence (SSCI), IEEE, 2017: 1-8. |

| [65] | LI H, SHEN Y, ZHU Y. Stock price prediction using attention-based multi-input LSTM[C]// Asian conference on machine learning, PMLR, 2018: 454-469. |

| [66] | ZHANG X, TAN Y. Deep stock ranker: A LSTM neural network model for stock selection[C]// Data Mining and Big Data: Third International Conference, DMBD 2018, Shanghai, China, June 17-22, 2018, Proceedings 3. Springer International Publishing, 2018: 614-623. |

| [67] | LAI C, CHEN R, CARAKA R.Prediction stock price based on different index factors using LSTM[C]//2019 International conference on machine learning and cybernetics (ICML-C), IEEE, 2019: 1-6 |

| [68] | 王鹭轩. 基于混合模型的股指期货研究与预测[D]. 大连理工大学, 2020. |

| [69] | LONG J, CHEN Z, HE W, et al. An integrated framework of deep learning and knowledge graph for prediction of stock price trend: An application in Chinese stock exchangemarket[J]. Applied Soft Computing, 2020, 91: 106205. |

| [70] | WANG J, ZHU S. A multi-factor two-stage deep integration model for stock price prediction based on intelligent optimization and feature clustering[J]. Artificial Intelligence Re-view, 2023, 56(7): 7237-7262. |

| [71] | 周全. CNN与LSTM在周期股短期股价涨跌预测的应用研究[D]. 浙江大学, 2023. |

| [72] | ZHAO C, HU P, LIU X, et al. Stock market analysis using time series relationnal models for stock price prediction[J]. Mathematics, 2023, 11(5): 1130. |

| [73] | 陈卫华. 基于深度学习的上证综指波动率预测效果比较研究[J]. 统计与信息论坛, 2018, 33(5): 99-106. |

| [74] | BARNDORFF O, HANSEN P, LUNDE A, et al. Designing Realized Kernels to Measure the expost Variation of equity Pricesin the Presence of Noise[J]. Econometrica, 2008, 76(6): 1481-1536. |

| [75] | 周子昂, 尚瑞琪. 沪深300高频波动率的预测及应用——基于深度学习的方法[J]. 上海立信会计金融学院学报, 2019(4): 60-74. |

| [76] | 吴鸿超. 基于深度学习LSTM模型的高频数据波动率预测及其在金融领域中的应用[D]. 南京审计大学, 2022. |

| [77] | 张颖芝. 高频数据下股票波动率预测[D]. 浙江工商大学, 2022. |

| [78] | 高玉嫣. 基于机器学习中LSTM模型对高频数据的已实现波动率预测研究[D]. 南京财经大学, 2023. |

| [79] | LONG W, LU Z, CUI L. Deep learning based feature engineering for stock price movement prediction[J]. Knowledge-Based Systems, 2019, 164: 163-173. |

| [80] | HU Z, LIU W, BIAN J, et al. Listening to chaotic whispers: A deep learning frameworkfor news-oriented stock trend prediction[C]// Proceedings of the eleventh ACM international conference on web search and data min-ing, 2018: 261-269. |

| [81] | JIA W, CHEN W, XIONG L, et al. Quantitative trading on stock market based on deepreinforcement learning[C]// 2019 International Joint Conference on Neural Networks (IJCNN), IEEE, 2019: 1-8. |

| [82] | 任佳屹, 王爱银. 融合因果注意力Transformer模型的股价预测研究[J]. 计算机工程与应用, 2023, 59(13): 325-334. |

| [83] | 陈建勋. 基于高频数据的中国股市日内回转交易研究[D]. 哈尔滨工业大学, 2019. |

| [84] | 陈紫晴. 基于机器学习方法对沪深300指数的涨跌预测研究[D]. 上海财经大学, 2023. |

| [85] | 牛进鹏. 基于EEMD-XGBoost机器学习方法的已实现波动率预测研究[D]. 东华大学, 2022. |

| [86] | 文馨贤. 融合经验模态分解与线性Transformer的高频金融时间序列预测[J]. 现代电子技术, 2022, 45(23): 121-126. |

| [87] | 朱峰. 基于深度学习的金融市场高频交易数据波动率预测的研究与应用[D]. 东华大学, 2023. |

| [88] | XU H, CHAI L, LUO Z, et al. Stock movement prediction via gated recurrent unit network based on reinforcement learning with incorporated attention mechanisms[J]. Neurocomputing, 2022, 467: 214-228. |

| [1] | JI Peng,NIU Tie,WEI Ting,PENG Liang. Research on Supercomputer Job Running State Prediction Based on XGBoost Model [J]. Frontiers of Data and Computing, 2024, 6(6): 123-129. |

| [2] | LONG Chun, LI Lisha, LI Jing, YANG Fan, WEI Jinxia, Fu Yuhao. Review of Research on Secure Inference in Machine Learning [J]. Frontiers of Data and Computing, 2024, 6(5): 1-12. |

| [3] | GUO Xuebing, ZHU Xiaojie, TANG Xinzhai, YANG Gang, HOU Yanfei, HE Honglin. Study on Integration Method of Algorithm Model Based on Big Data Pipeline— Taking Tree Biomass Inversion Based on Machine Learning Method and LiDAR Data as an Example [J]. Frontiers of Data and Computing, 2024, 6(4): 96-105. |

| [4] | HE Ruilin, YANG Xinyi, SUN Hongzan, LI Chen. The Latest Development and Prospects of Histopathological Image Analysis Methods Based on Graph Features [J]. Frontiers of Data and Computing, 2024, 6(2): 101-116. |

| [5] | YE Xu, DU Yi, CUI Wenjuan, SHEN Junjie, XIE Jing, WANG Ludi. Application of Machine Learning Technology in the Field of Eye Health [J]. Frontiers of Data and Computing, 2024, 6(2): 117-133. |

| [6] | SHEN Zhihao, LI Na, YIN Shihao, DU Yi, HU Lianglin. Airfare Price Prediction Based on TPA-Transformer [J]. Frontiers of Data and Computing, 2023, 5(6): 115-125. |

| [7] | WEI Ting, PENG Liang, NIU Tie, ZHANG Honghai. Detection and Root Cause Analysis of HPC Failure Jobs Based on Feature Analysis [J]. Frontiers of Data and Computing, 2023, 5(6): 94-103. |

| [8] | SUN Yifan, ZHANG Rui, TAO Yang, GAO Birou, QIN Shihan, AN Chao. A Survey on Local Differential Privacy [J]. Frontiers of Data and Computing, 2023, 5(5): 74-97. |

| [9] | TIAN Yiqing, CHENG Xi, FENG Bojing. A Review of Computational Models for Corporate Credit Rating [J]. Frontiers of Data and Computing, 2023, 5(4): 139-153. |

| [10] | CHEN Meilin, LIU Duanyang, XU Liming, WANG Yang. A Review of Force Field Models Based on Machine Learning [J]. Frontiers of Data and Computing, 2023, 5(4): 27-37. |

| [11] | LIU Duanyang, WEI Zhongming. Application of Supervised Learning Algorithms in Materials Science [J]. Frontiers of Data and Computing, 2023, 5(4): 38-47. |

| [12] | LI Yan,HE Hongbo,WANG Runqiang. A Survey of Research on Microblog Popularity Prediction [J]. Frontiers of Data and Computing, 2023, 5(2): 119-135. |

| [13] | GAO Tian,ZHU Jiaojun,ZHANG Jinxin,SUN Yirong,YU Fengyuan,TENG Dexiong,LU Deliang,YU Lizhong,WANG Zongguo. Estimation of Carbon Flux of a Temperate Forest Ecosystem Based on Next-Generation Information Technologies [J]. Frontiers of Data and Computing, 2023, 5(2): 60-72. |

| [14] | WANG Fan,FENG Liqiang,CAO Rongqiang. Design and Application of Big Data-Driven Ocean Artificial Intelligence Service Platform [J]. Frontiers of Data and Computing, 2023, 5(2): 73-85. |

| [15] | ZHAO Zhongbin,CAI Manchun,LU Tianliang. Network Malicious Traffic Detection Incorporating Multi-Head Attention Mechanism [J]. Frontiers of Data and Computing, 2022, 4(5): 60-67. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||