数据与计算发展前沿 ›› 2026, Vol. 8 ›› Issue (1): 45-63.

CSTR: 32002.14.jfdc.CN10-1649/TP.2026.01.005

doi: 10.11871/jfdc.issn.2096-742X.2026.01.005

冯文君1( ),张正军2,3,4,*(),王一鸣5

),张正军2,3,4,*(),王一鸣5

收稿日期:2025-03-20

出版日期:2026-02-20

发布日期:2026-02-02

通讯作者:

张正军

作者简介:冯文君,北京交通大学经济管理学院,讲师,主要研究方向为金融科技。基金资助:

FENG Wenjun1(),ZHANG Zhengjun2,3,4,*(),WANG Yiming5

Received:2025-03-20

Online:2026-02-20

Published:2026-02-02

Contact:

ZHANG Zhengjun

摘要:

【目的】探讨股价跳跃特征与机器学习模型在已实现波动率预测中的协同作用,分析不同预测方法在不同时间尺度上的表现。【方法】基于上证50指数成分股2019年至2024年的五分钟高频数据,采用阈值法逐点识别股价跳跃,并通过K-近邻算法(KNN)提取跳跃频率、跳跃幅度等多维特征,构建包含丰富跳跃信息的特征体系。随后,使用扩展的异质自回归波动率(HAR)模型及10种机器学习算法,包括KNN、随机森林(RF)、梯度提升回归树(GBRT)、支持向量回归(SVR)等,对多周期已实现波动率进行预测,并系统评估机器学习方法与跳跃信息的结合效果。【结果】样本内预测显示,引入跳跃特征与采用机器学习模型均能提高预测精度,其中KNN与随机森林的表现最优。在样本外预测中,HAR-RV模型在日度预测中仍然最优,而在周度和月度预测中,跳跃信息和机器学习模型可提升预测效果,但当HAR模型已整合跳跃信息后,机器学习方法未能进一步改善预测性能。【结论】本研究扩展了波动率预测的特征空间,并系统评估了机器学习方法在波动率预测中的有效性。研究表明,多维跳跃特征能够提供额外信息,有助于提高中长期波动率预测精度。然而在HAR模型已纳入跳跃信息后, 机器学习模型难以进一步提供增量价值。这一发现对金融市场风险管理和资产定价具有重要意义。

冯文君,张正军,王一鸣. 跳跃信息、机器学习模型与已实现波动率预测[J]. 数据与计算发展前沿, 2026, 8(1): 45-63.

FENG Wenjun,ZHANG Zhengjun,WANG Yiming. Jump Information, Machine Learning Models, and Realized Volatility Forecasting[J]. Frontiers of Data and Computing, 2026, 8(1): 45-63, https://cstr.cn/32002.14.jfdc.CN10-1649/TP.2026.01.005.

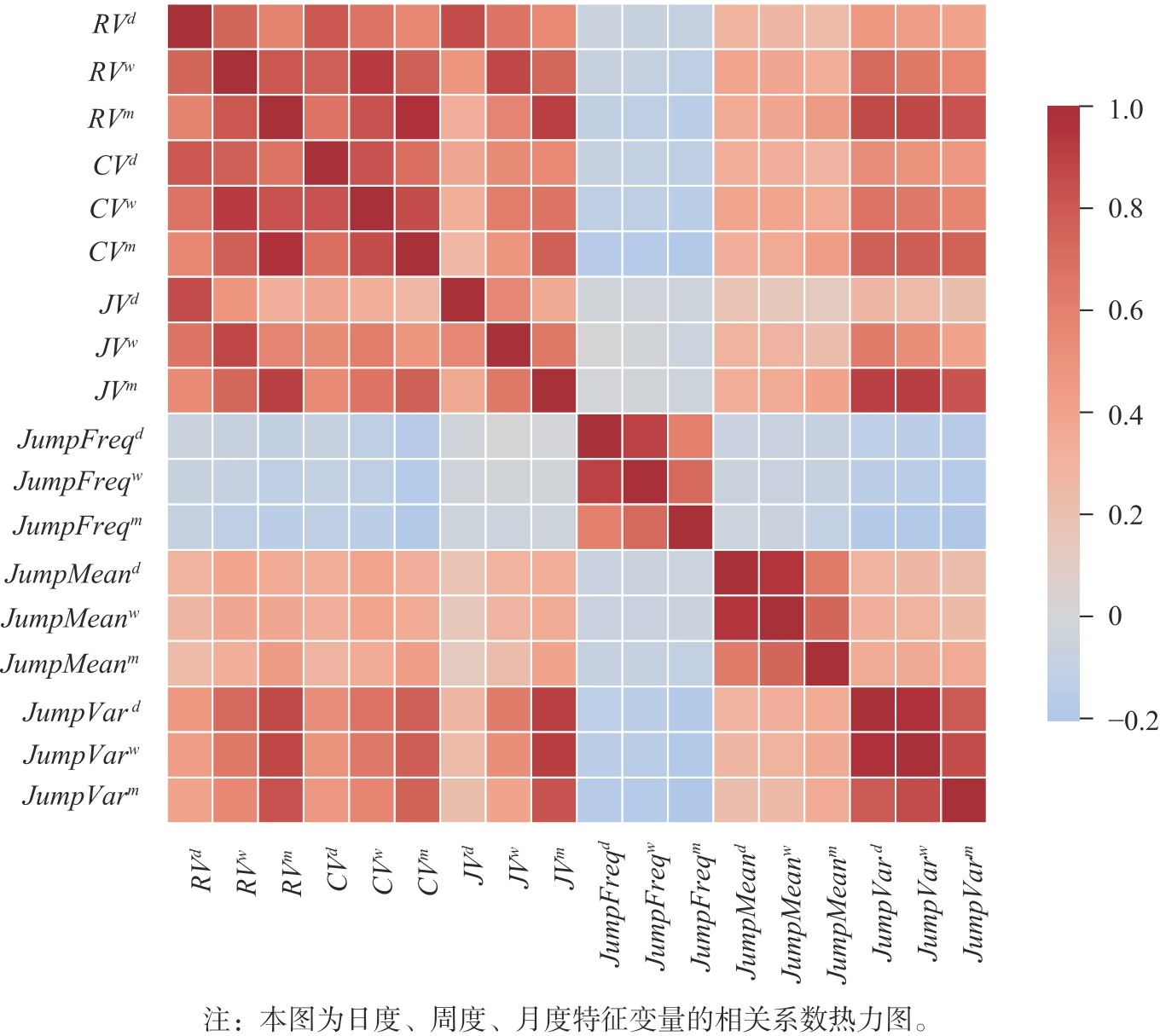

表1

描述性统计"

| 均值 | 0.1504 | 0.0942 | 0.0562 | 1.2032 | 0.0018 | 0.0002 |

| 标准差 | 0.2392 | 0.1336 | 0.1541 | 0.3667 | 0.0036 | 0.0002 |

| 偏度 | 6.0572 | 6.7248 | 8.6674 | 4.6229 | 1.0929 | 3.2598 |

| 峰度 | 65.8597 | 118.5584 | 111.8555 | 65.7323 | 4.2289 | 18.6625 |

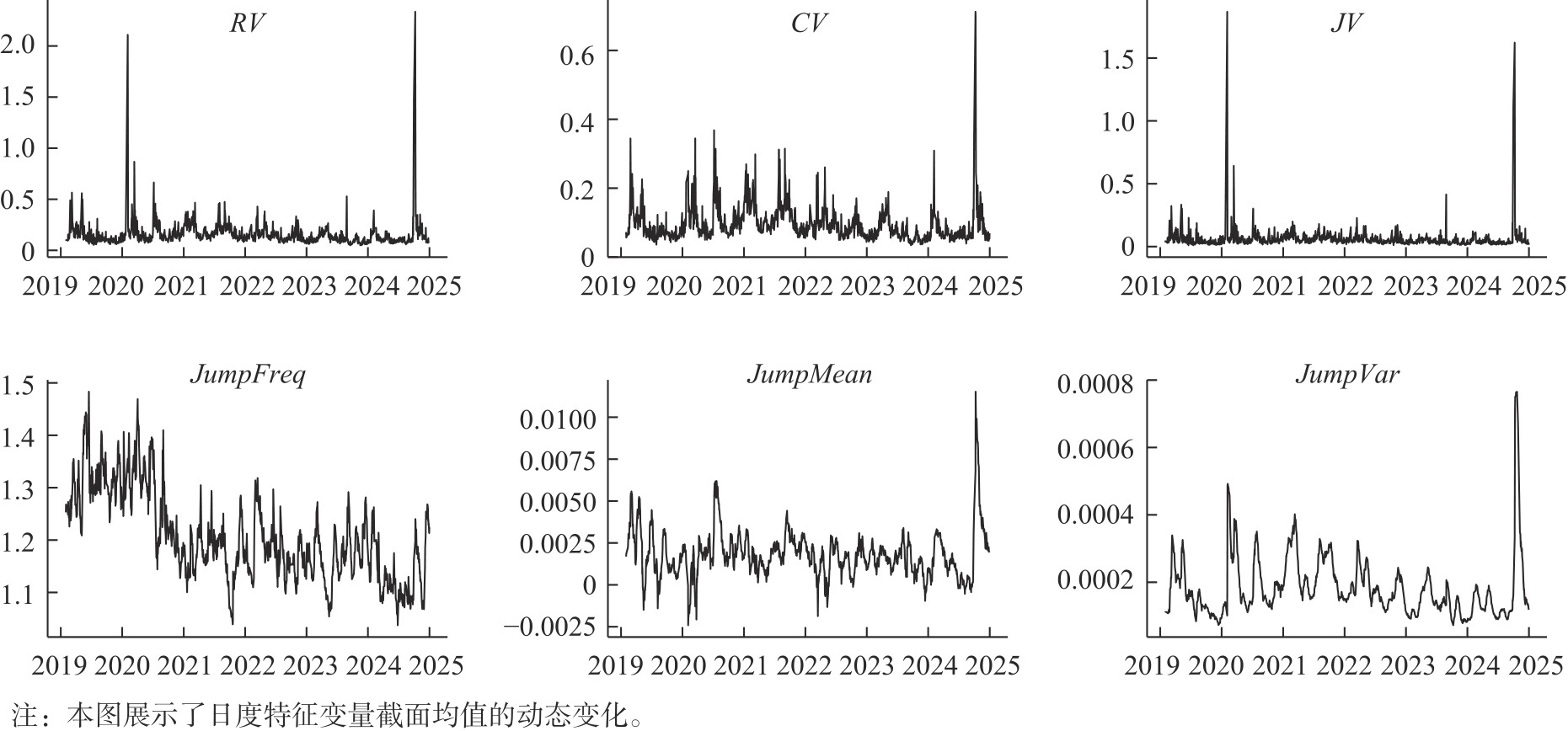

图1

特征变量截面均值的动态变化"

表2

特征变量相关性"

| 1.0000 | 0.8033 | 0.8564 | -0.0551 | 0.2990 | 0.4687 | |

| 0.8033 | 1.0000 | 0.3805 | -0.0791 | 0.3347 | 0.5220 | |

| 0.8564 | 0.3805 | 1.0000 | -0.0169 | 0.1742 | 0.2753 | |

| -0.0551 | -0.0791 | -0.0169 | 1.0000 | -0.0590 | -0.1377 | |

| 0.2990 | 0.3347 | 0.1742 | -0.0590 | 1.0000 | 0.2956 | |

| 0.4687 | 0.5220 | 0.2753 | -0.1377 | 0.2956 | 1.0000 |

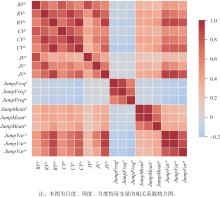

图2

特征变量相关性热力图"

表3

HAR模型回归结果"

| 特征集1 | 特征集2 | 特征集3 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 日度 | 周度 | 月度 | 日度 | 周度 | 月度 | 日度 | 周度 | 月度 | |||||||

| 0.2734 | 0.1525 | 0.0713 | |||||||||||||

| (78.6610) | (63.4492) | (35.0318) | |||||||||||||

| 0.2923 | 0.2508 | 0.1587 | |||||||||||||

| (47.8187) | (59.2061) | (44.2755) | |||||||||||||

| 0.3045 | 0.3980 | 0.4490 | |||||||||||||

| (50.8216) | (96.0699) | (127.1862) | |||||||||||||

| 0.4336 | 0.2857 | 0.1592 | 0.5141 | 0.3260 | 0.1717 | ||||||||||

| (58.0161) | (55.9997) | (36.8528) | (67.7052) | (63.6538) | (40.0368) | ||||||||||

| 0.4541 | 0.4659 | 0.3306 | 0.4968 | 0.4781 | 0.3495 | ||||||||||

| (35.4831) | (53.4516) | (44.9044) | (37.4969) | (53.6447) | (46.9145) | ||||||||||

| 0.2459 | 0.3664 | 0.5105 | 0.1857 | 0.3366 | 0.4824 | ||||||||||

| (18.8515) | (41.3923) | (68.2617) | (13.0054) | (35.1333) | (60.2734) | ||||||||||

| 0.2167 | 0.1076 | 0.0418 | |||||||||||||

| (49.9777) | (36.5844) | (16.9186) | |||||||||||||

| 0.0851 | 0.0146 | -0.0141 | |||||||||||||

| (8.5830) | (2.1656) | (-2.5003) | |||||||||||||

| 0.1250 | 0.1453 | 0.1080 | |||||||||||||

| (7.6911) | (13.2157) | (11.5782) | |||||||||||||

| 0.0143 | 0.0066 | 0.0016 | |||||||||||||

| (13.1505) | (9.0509) | (2.7059) | |||||||||||||

| -0.0143 | -0.0075 | -0.0030 | |||||||||||||

| (-11.4261) | (-9.0194) | (-4.2963) | |||||||||||||

| 0.0068 | 0.0062 | 0.0046 | |||||||||||||

| (13.6450) | (18.6392) | (16.4187) | |||||||||||||

| 0.0184 | 0.0275 | 0.0431 | 0.0183 | 0.0274 | 0.0431 | 0.0199 | 0.0271 | 0.0420 | |||||||

| (25.2712) | (54.4080) | (99.4040) | (25.4306) | (55.9343) | (103.2671) | (26.7838) | (54.3054) | (99.7796) | |||||||

| 特征集4 | 特征集5 | 特征集6 | |||||||||||||

| 日度 | 周度 | 月度 | 日度 | 日度 | 周度 | 日度 | 周度 | 月度 | |||||||

| 0.4272 | 0.2856 | 0.1592 | 0.5034 | 0.3197 | 0.1682 | 0.4175 | 0.2775 | 0.1523 | |||||||

| (56.3962) | (55.4185) | (36.6144) | (66.0931) | (62.2559) | (39.1062) | (54.8244) | (53.6412) | (34.9005) | |||||||

| 0.4522 | 0.4501 | 0.3321 | 0.4705 | 0.4525 | 0.3298 | 0.4502 | 0.4495 | 0.3336 | |||||||

| (34.7662) | (50.9433) | (44.6581) | (34.9462) | (50.0077) | (43.5800) | (33.4197) | (49.2446) | (43.4262) | |||||||

| 0.2506 | 0.3777 | 0.5028 | 0.2089 | 0.3577 | 0.5010 | 0.2465 | 0.3676 | 0.4978 | |||||||

| (18.6824) | (41.5738) | (65.7440) | (14.2549) | (36.4172) | (60.9695) | (16.8316) | (37.1693) | (59.8158) | |||||||

| 0.2167 | 0.1077 | 0.0412 | 0.2195 | 0.1094 | 0.0401 | ||||||||||

| (49.5984) | (36.4575) | (16.7035) | (46.5816) | (34.3912) | (15.0598) | ||||||||||

| 0.0820 | 0.0128 | -0.0183 | 0.0445 | -0.0119 | -0.0314 | ||||||||||

| (8.1884) | (1.8895) | (-3.2349) | (3.2625) | (-1.2940) | (-4.0535) | ||||||||||

| 0.1254 | 0.1460 | 0.1162 | 0.1623 | 0.1600 | 0.1543 | ||||||||||

| (7.5664) | (13.0498) | (12.2982) | (5.3835) | (7.8725) | (8.8742) | ||||||||||

| 0.0000 | 0.0000 | 0.0000 | 0.0001 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |||||||

| (1.2917) | (1.2371) | (0.5601) | (4.7611) | (3.7361) | (1.5766) | (2.2217) | (2.3581) | (1.2465) | |||||||

| -0.0000 | -0.0000 | -0.0000 | -0.0001 | -0.0000 | -0.0000 | -0.0000 | -0.0000 | -0.0000 | |||||||

| (-1.2144) | (-1.3253) | (-2.7100) | (-3.2754) | (-2.6284) | (-3.0625) | (-2.3008) | (-2.6519) | (-3.8601) | |||||||

| -0.0000 | -0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |||||||

| (-0.3299) | (-0.8672) | (0.7395) | (1.8109) | (1.8434) | (2.8658) | (0.2245) | (0.2193) | (1.4829) | |||||||

| 0.0006 | 0.0004 | 0.0003 | 0.0005 | 0.0004 | 0.0003 | ||||||||||

| (16.1214) | (16.5137) | (12.6899) | (12.4428) | (14.1834) | (11.9258) | ||||||||||

| -0.0005 | -0.0003 | -0.0002 | -0.0004 | -0.0003 | -0.0002 | ||||||||||

| (-11.6082) | (-9.9204) | (-6.7699) | (-8.9154) | (-8.4847) | (-6.7614) | ||||||||||

| 0.0000 | -0.0000 | -0.0001 | 0.0000 | -0.0000 | -0.0001 | ||||||||||

| (1.6767) | (-1.6169) | (-4.3002) | (0.2314) | (-2.6681) | (-4.6811) | ||||||||||

| 0.0151 | 0.0071 | 0.0020 | 0.0056 | 0.0044 | 0.0022 | ||||||||||

| (13.9102) | (9.7267) | (3.2656) | (3.8549) | (4.4793) | (2.6889) | ||||||||||

| -0.0149 | -0.0080 | -0.0034 | -0.0093 | -0.0082 | -0.0061 | ||||||||||

| (-11.9530) | (-9.5473) | (-4.8554) | (-5.7842) | (-7.5661) | (-6.6299) | ||||||||||

| 0.0066 | 0.0062 | 0.0047 | 0.0042 | 0.0049 | 0.0040 | ||||||||||

| (13.2639) | (18.4812) | (16.5241) | (8.2981) | (14.3489) | (13.8061) | ||||||||||

| 0.0202 | 0.0301 | 0.0478 | 0.0091 | 0.0204 | 0.0412 | 0.0184 | 0.0273 | 0.0469 | |||||||

| (7.7037) | (16.9986) | (31.8340) | (3.4123) | (11.3901) | (27.2933) | (6.4147) | (14.1187) | (28.6104) | |||||||

表4

样本内预测的R2"

| 预测周期 | 日度RV | |||||

|---|---|---|---|---|---|---|

| 特征集 | 1 | 2 | 3 | 4 | 5 | 6 |

| HAR | 0.3831 | 0.3974 | 0.3826 | 0.3975 | 0.3835 | 0.3989 |

| LASSO | 0.3831 | 0.3974 | 0.3826 | 0.3975 | 0.3835 | 0.3988 |

| PCR | 0.3815 | 0.3970 | 0.3826 | 0.3970 | 0.3835 | 0.3989 |

| KNN | 0.4318 | 0.4393 | 0.4263 | 0.4373 | 0.4334 | 0.4469 |

| RF | 0.4106 | 0.4738 | 0.4952 | 0.4598 | 0.4607 | 0.5049 |

| GBRT | 0.3438 | 0.3404 | 0.3260 | 0.3446 | 0.3258 | 0.3327 |

| TCN | 0.3943 | 0.4201 | 0.3910 | 0.4172 | 0.3992 | 0.4236 |

| SVR | 0.3417 | 0.3526 | 0.3452 | 0.3524 | 0.3463 | 0.3537 |

| NN | 0.3942 | 0.3995 | 0.3839 | 0.4048 | 0.3899 | 0.4167 |

| LSTM | 0.4065 | 0.4232 | 0.4002 | 0.4437 | 0.4368 | 0.4647 |

| Transformer | 0.3653 | 0.3945 | 0.3844 | 0.4009 | 0.4016 | 0.4183 |

| 预测周期 | 周度 | |||||

| 特征集 | 1 | 2 | 3 | 4 | 5 | 6 |

| HAR | 0.5037 | 0.5330 | 0.5266 | 0.5331 | 0.5281 | 0.5353 |

| LASSO | 0.5037 | 0.5330 | 0.5266 | 0.5330 | 0.5281 | 0.5352 |

| PCR | 0.5033 | 0.5330 | 0.5266 | 0.5331 | 0.5272 | 0.5345 |

| KNN | 0.5599 | 0.5787 | 0.5847 | 0.5899 | 0.6315 | 0.6241 |

| RF | 0.5460 | 0.5884 | 0.6012 | 0.5812 | 0.6199 | 0.6470 |

| GBRT | 0.4554 | 0.4569 | 0.4475 | 0.4620 | 0.4496 | 0.4479 |

| TCN | 0.5331 | 0.5526 | 0.5275 | 0.5451 | 0.5644 | 0.5762 |

| SVR | 0.4495 | 0.4679 | 0.4647 | 0.4684 | 0.4650 | 0.4697 |

| NN | 0.5312 | 0.5430 | 0.5386 | 0.5427 | 0.5335 | 0.5436 |

| LSTM | 0.5373 | 0.5607 | 0.5518 | 0.5757 | 0.5997 | 0.6070 |

| Transformer | 0.4950 | 0.5419 | 0.5306 | 0.5411 | 0.5472 | 0.5534 |

| 预测周期 | 月度 | |||||

| 特征集 | 1 | 2 | 3 | 4 | 5 | 6 |

| HAR | 0.5169 | 0.5526 | 0.5518 | 0.5528 | 0.5531 | 0.5550 |

| LASSO | 0.5168 | 0.5526 | 0.5517 | 0.5523 | 0.5520 | 0.5535 |

| PCR | 0.5169 | 0.5525 | 0.5517 | 0.5526 | 0.5525 | 0.5540 |

| KNN | 0.5834 | 0.6107 | 0.6319 | 0.6319 | 0.7058 | 0.6920 |

| RF | 0.5740 | 0.6095 | 0.6152 | 0.5937 | 0.6582 | 0.6539 |

| GBRT | 0.4731 | 0.4800 | 0.4803 | 0.4872 | 0.4796 | 0.4743 |

| TCN | 0.5576 | 0.5755 | 0.5899 | 0.5941 | 0.6492 | 0.6482 |

| SVR | 0.4420 | 0.4693 | 0.4704 | 0.4713 | 0.4709 | 0.4713 |

| NN | 0.5357 | 0.5705 | 0.5632 | 0.5721 | 0.5743 | 0.5752 |

| LSTM | 0.5591 | 0.5881 | 0.5960 | 0.6113 | 0.6598 | 0.6663 |

| Transformer | 0.5036 | 0.5711 | 0.5718 | 0.5760 | 0.6144 | 0.6787 |

表5

样本内预测Diebold-Mariano检验[22]p值"

| 预测周期 | 日度RV | |||||

|---|---|---|---|---|---|---|

| 特征集 | 1 | 2 | 3 | 4 | 5 | 6 |

| HAR | 0.0001 | 0.5189 | 0.0001 | 0.4861 | 0.0000 | |

| LASSO | 0.4462 | 0.0001 | 0.5181 | 0.0002 | 0.4844 | 0.0000 |

| PCR | 0.7517 | 0.0004 | 0.5189 | 0.0005 | 0.4861 | 0.0000 |

| KNN | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| RF | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| GBRT | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| TCN | 0.0262 | 0.0000 | 0.1074 | 0.0002 | 0.0024 | 0.0040 |

| SVR | 1.0000 | 0.9986 | 0.9994 | 0.9984 | 0.9992 | 0.9980 |

| NN | 0.0001 | 0.0039 | 0.4669 | 0.0000 | 0.1851 | 0.0007 |

| LSTM | 0.0001 | 0.0000 | 0.0023 | 0.0000 | 0.0000 | 0.0000 |

| Transformer | 1.0000 | 0.0090 | 0.4505 | 0.0000 | 0.0099 | 0.0115 |

| 预测周期 | 周度 | |||||

| 特征集 | 1 | 2 | 3 | 4 | 5 | 6 |

| HAR | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| LASSO | 0.4195 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| PCR | 0.7605 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| KNN | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| RF | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| GBRT | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| TCN | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| SVR | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| NN | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| LSTM | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Transformer | 0.9989 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| 预测周期 | 月度 | |||||

| 特征集 | 1 | 2 | 3 | 4 | 5 | 6 |

| HAR | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| LASSO | 0.5838 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| PCR | 0.7624 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| KNN | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| RF | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| GBRT | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| TCN | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| SVR | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| NN | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| LSTM | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Transformer | 1.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

表6

样本外预测的 R o o s 2"

| 预测周期 | 日度 | |||||

|---|---|---|---|---|---|---|

| 特征集 | 1 | 2 | 3 | 4 | 5 | 6 |

| HAR | 0.3128 | 0.3028 | 0.2620 | 0.3012 | 0.2605 | 0.3009 |

| LASSO | 0.2754 | 0.2515 | 0.2469 | 0.2505 | 0.2469 | 0.2505 |

| PCR | 0.2947 | 0.2834 | 0.2474 | 0.2825 | 0.2463 | 0.2754 |

| KNN | 0.2767 | 0.2523 | 0.2443 | 0.2485 | 0.2272 | 0.2535 |

| RF | 0.2797 | 0.2741 | 0.2446 | 0.2709 | 0.2316 | 0.2573 |

| GBRT | 0.2366 | 0.2350 | 0.2208 | 0.2380 | 0.2199 | 0.2265 |

| TCN | 0.3125 | 0.2809 | 0.2560 | 0.2786 | 0.2408 | 0.2892 |

| SVR | 0.2599 | 0.2423 | 0.2316 | 0.2418 | 0.2332 | 0.2434 |

| NN | 0.3069 | 0.2917 | 0.2554 | 0.2864 | 0.2630 | 0.3091 |

| LSTM | 0.3056 | 0.2998 | 0.2644 | 0.2681 | 0.2375 | 0.2450 |

| Transformer | 0.3022 | 0.2767 | 0.2439 | 0.2947 | 0.2273 | 0.2707 |

| 预测周期 | 周度 | |||||

| 特征集 | 1 | 2 | 3 | 4 | 5 | 6 |

| HAR | 0.2714 | 0.3086 | 0.2930 | 0.3094 | 0.2851 | 0.2997 |

| LASSO | 0.2556 | 0.2765 | 0.2786 | 0.2788 | 0.2786 | 0.2771 |

| PCR | 0.2472 | 0.2735 | 0.2602 | 0.2771 | 0.2532 | 0.2668 |

| KNN | 0.2640 | 0.2461 | 0.2538 | 0.2480 | 0.2207 | 0.2307 |

| RF | 0.2930 | 0.2880 | 0.2717 | 0.2855 | 0.2396 | 0.2557 |

| GBRT | 0.2633 | 0.2687 | 0.2609 | 0.2756 | 0.2595 | 0.2597 |

| TCN | 0.3048 | 0.3072 | 0.2912 | 0.2789 | 0.2605 | 0.2647 |

| SVR | 0.2359 | 0.2403 | 0.2331 | 0.2414 | 0.2334 | 0.2408 |

| NN | 0.3175 | 0.3023 | 0.2982 | 0.2992 | 0.2913 | 0.2898 |

| LSTM | 0.3069 | 0.2589 | 0.2488 | 0.2455 | 0.2039 | 0.1459 |

| Transformer | 0.2443 | 0.2768 | 0.2642 | 0.2845 | 0.2514 | 0.2754 |

| 预测周期 | 月度RV | |||||

| 特征集 | 1 | 2 | 3 | 4 | 5 | 6 |

| HAR | 0.2098 | 0.3014 | 0.2934 | 0.3015 | 0.2668 | 0.2698 |

| LASSO | 0.1930 | 0.2672 | 0.2700 | 0.2719 | 0.2700 | 0.2533 |

| PCR | 0.1487 | 0.2255 | 0.2236 | 0.2320 | 0.2052 | 0.2066 |

| KNN | 0.2069 | 0.1990 | 0.2130 | 0.1858 | 0.1262 | 0.1433 |

| RF | 0.2669 | 0.2789 | 0.2580 | 0.2822 | 0.2370 | 0.2506 |

| GBRT | 0.2745 | 0.2812 | 0.2798 | 0.2914 | 0.2775 | 0.2729 |

| TCN | 0.2990 | 0.2560 | 0.2851 | 0.2233 | 0.1912 | 0.2536 |

| SVR | 0.1550 | 0.1949 | 0.1925 | 0.1993 | 0.1884 | 0.1903 |

| NN | 0.2119 | 0.2556 | 0.2373 | 0.2747 | 0.2657 | 0.2569 |

| LSTM | 0.3076 | 0.2759 | 0.2654 | 0.2039 | 0.1172 | 0.1593 |

| Transformer | 0.2062 | 0.2582 | 0.2109 | 0.2335 | 0.0569 | 0.1486 |

表7

样本外预测Diebold-Mariano检验[22]p值"

| 预测周期 | 日度RV | |||||

|---|---|---|---|---|---|---|

| 特征集 | 1 | 2 | 3 | 4 | 5 | 6 |

| HAR | 0.7153 | 0.9061 | 0.7317 | 0.9166 | 0.7463 | |

| LASSO | 0.9941 | 0.9582 | 0.9577 | 0.9558 | 0.9576 | 0.9558 |

| PCR | 1.0000 | 0.9588 | 0.9699 | 0.9519 | 0.9746 | 0.9711 |

| KNN | 0.9968 | 0.9973 | 0.9927 | 0.9924 | 0.9956 | 0.9914 |

| RF | 0.9396 | 0.9740 | 0.9763 | 0.9595 | 0.9906 | 0.9807 |

| GBRT | 0.9843 | 0.9811 | 0.9843 | 0.9758 | 0.9846 | 0.9841 |

| TCN | 0.5088 | 0.9440 | 0.9624 | 0.9690 | 0.9901 | 0.8832 |

| SVR | 0.9953 | 0.9796 | 0.9812 | 0.9790 | 0.9801 | 0.9779 |

| NN | 0.6673 | 0.8200 | 0.9608 | 0.9407 | 0.9250 | 0.5955 |

| LSTM | 0.6684 | 0.8122 | 0.9449 | 0.9953 | 0.9928 | 0.9998 |

| Transformer | 0.9970 | 0.9888 | 0.9866 | 0.8265 | 0.9970 | 0.9152 |

| 预测周期 | 周度RV | |||||

| 特征集 | 1 | 2 | 3 | 4 | 5 | 6 |

| HAR | 0.0030 | 0.1587 | 0.0038 | 0.2460 | 0.0164 | |

| LASSO | 0.9045 | 0.4049 | 0.3704 | 0.3660 | 0.3704 | 0.3844 |

| PCR | 0.9997 | 0.4322 | 0.7280 | 0.3282 | 0.8548 | 0.6413 |

| KNN | 0.6793 | 0.9384 | 0.8350 | 0.9379 | 0.9981 | 0.9991 |

| RF | 0.1037 | 0.1616 | 0.4932 | 0.1972 | 0.9606 | 0.8565 |

| GBRT | 0.6361 | 0.5447 | 0.6564 | 0.4306 | 0.6784 | 0.6819 |

| TCN | 0.0270 | 0.0118 | 0.1344 | 0.2906 | 0.7380 | 0.6721 |

| SVR | 0.9861 | 0.9264 | 0.9542 | 0.9177 | 0.9560 | 0.9255 |

| NN | 0.0018 | 0.0016 | 0.0805 | 0.0304 | 0.1227 | 0.1213 |

| LSTM | 0.0077 | 0.8341 | 0.9393 | 0.9579 | 1.0000 | 1.0000 |

| Transformer | 0.9998 | 0.3099 | 0.6649 | 0.1935 | 0.9126 | 0.3577 |

| 预测周期 | 月度RV | |||||

| 特征集 | 1 | 2 | 3 | 4 | 5 | 6 |

| HAR | 0.0000 | 0.0000 | 0.0000 | 0.0007 | 0.0001 | |

| LASSO | 0.8790 | 0.0026 | 0.0019 | 0.0012 | 0.0019 | 0.0117 |

| PCR | 1.0000 | 0.1461 | 0.2286 | 0.0644 | 0.6082 | 0.5840 |

| KNN | 0.5693 | 0.7063 | 0.4352 | 0.9145 | 1.0000 | 1.0000 |

| RF | 0.0012 | 0.0003 | 0.0115 | 0.0001 | 0.0844 | 0.0212 |

| GBRT | 0.0097 | 0.0056 | 0.0061 | 0.0016 | 0.0058 | 0.0110 |

| TCN | 0.0000 | 0.0089 | 0.0002 | 0.2714 | 0.7970 | 0.0209 |

| SVR | 0.9937 | 0.7117 | 0.7390 | 0.6534 | 0.7924 | 0.7705 |

| NN | 0.4388 | 0.0074 | 0.0897 | 0.0002 | 0.0040 | 0.0050 |

| LSTM | 0.0000 | 0.0004 | 0.0047 | 0.6551 | 0.9998 | 0.9739 |

| Transformer | 0.6040 | 0.0029 | 0.4732 | 0.1100 | 1.0000 | 0.9910 |

| [1] |

CORSI F. A simple approximate long-memory model of realized volatility[J]. Journal of Financial Econometrics, 2009, 7(2): 174-196.

doi: 10.1093/jjfinec/nbp001 |

| [2] |

ANDERSEN T G, BOLLERSLEV T, DIEBOLD F X. Roughing it up: Including jump components in the measurement, modeling, and forecasting of return volatility[J]. The Review of Economics and Statistics, 2007, 89(4): 701-720.

doi: 10.1162/rest.89.4.701 |

| [3] |

BOLLERSLEV T, TODOROV V, LI S Z. Jump tails, extreme dependencies, and the distribution of stock returns[J]. Journal of Econometrics, 2013, 172(2): 307-324.

doi: 10.1016/j.jeconom.2012.08.014 |

| [4] |

CAPORIN M. The role of jumps in realized volatility modeling and forecasting[J]. Journal of Financial Econometrics, 2023, 21(4): 1143-1168.

doi: 10.1093/jjfinec/nbab030 |

| [5] |

MERTON R C. Option pricing when underlying stock returns are discontinuous[J]. Journal of Financial Economics, 1976, 3(1-2): 125-144.

doi: 10.1016/0304-405X(76)90022-2 |

| [6] | AIT-SAHALIA Y, CACHO-DIAZ J, HURD T R. Portfolio choice with jumps: a closed-form solution[J]. The Annals of Applied Probability, 2009, 19(2): 556-584. |

| [7] |

AÏT-SAHALIA Y, CACHO-DIAZ J, LAEVEN R J A. Modeling financial contagion using mutually exciting jump processes[J]. Journal of Financial Economics, 2015, 117(3): 585-606.

doi: 10.1016/j.jfineco.2015.03.002 |

| [8] |

MAHEU J M, MCCURDY T H. News arrival, jump dynamics, and volatility components for individual stock returns[J]. The Journal of Finance, 2004, 59(2): 755-793.

doi: 10.1111/jofi.2004.59.issue-2 |

| [9] |

GU S, KELLY B, XIU D. Empirical asset pricing via machine learning[J]. The Review of Financial Studies, 2020, 33(5): 2223-2273.

doi: 10.1093/rfs/hhaa009 |

| [10] |

JIANG J, KELLY B, XIU D. (Re-) Imag (in) ing price trends[J]. The Journal of Finance, 2023, 78(6): 3193-3249.

doi: 10.1111/jofi.v78.6 |

| [11] |

CHEN L, PELGER M, ZHU J. Deep learning in asset pricing[J]. Management Science, 2024, 70(2): 714-750.

doi: 10.1287/mnsc.2023.4695 |

| [12] |

BUCCI A. Realized volatility forecasting with neural networks[J]. Journal of Financial Econometrics, 2020, 18(3): 502-531.

doi: 10.1093/jjfinec/nbaa008 |

| [13] |

ZHU H, BAI L, HE L, et al. Forecasting realized volatility with machine learning: Panel data perspective[J]. Journal of Empirical Finance, 2023, 73: 251-271.

doi: 10.1016/j.jempfin.2023.07.003 |

| [14] |

CHRISTENSEN K, SIGGAARD M, VELIYEV B. A machine learning approach to volatility forecasting[J]. Journal of Financial Econometrics, 2023, 21(5): 1680-1727.

doi: 10.1093/jjfinec/nbac020 |

| [15] |

LI S Z, TANG Y. Automated volatility forecasting[J]. Management Science, 2025, 71(7): 6248-6274.

doi: 10.1287/mnsc.2023.01520 |

| [16] |

ZHANG Y, SONG Y, PENG Y, et al. Volatility forecasting incorporating intraday positive and negative jumps based on deep learning model[J]. Journal of Forecasting, 2024, 43(7): 2749-2765.

doi: 10.1002/for.v43.7 |

| [17] |

ANDERSEN T G, BOLLERSLEV T, DIEBOLD F X, et al. The distribution of realized stock return volatility[J]. Journal of Financial Economics, 2001, 61(1): 43-76.

doi: 10.1016/S0304-405X(01)00055-1 |

| [18] |

BARNDORFF-NIELSEN O E, SHEPHARD N. Power and bipower variation with stochastic volatility and jumps[J]. Journal of Financial Econometrics, 2004, 2(1): 1-37.

doi: 10.1093/jjfinec/nbh001 |

| [19] | SILVERMAN B W. Density estimation for statistics and data analysis[M]. New York: Routledge, 2018. |

| [20] |

DING Z, GRANGER C W J, ENGLE R F. A long memory property of stock market returns and a new model[J]. Journal of Empirical Finance, 1993, 1(1): 83-106.

doi: 10.1016/0927-5398(93)90006-D |

| [21] |

TIBSHIRANI R. Regression shrinkage and selection via the lasso[J]. Journal of the Royal Statistical Society Series B: Statistical Methodology, 1996, 58(1): 267-288.

doi: 10.1111/j.2517-6161.1996.tb02080.x |

| [22] |

DIEBOLD F X, MARIANO R S. Comparing predictive accuracy[J]. Journal of Business & Economic Statistics, 2002, 20(1): 134-144.

doi: 10.1198/073500102753410444 |

| [23] |

LIU L Y, PATTON A J, SHEPPARD K. Does anything beat 5-minute RV? A comparison of realized measures across multiple asset classes[J]. Journal of Econometrics, 2015, 187(1): 293-311.

doi: 10.1016/j.jeconom.2015.02.008 |

| [24] |

Bollerslev T, Patton A J, Quaedvlieg R. Exploiting the errors: A simple approach for improved volatility forecasting[J]. Journal of Econometrics, 2016, 192(1): 1-18.

doi: 10.1016/j.jeconom.2015.10.007 |

| [25] |

BOLLERSLEV T, MEDEIROS M C, PATTON A J, et al. From zero to hero: Realized partial (co) variances[J]. Journal of Econometrics, 2022, 231(2): 348-360.

doi: 10.1016/j.jeconom.2021.04.013 |

| [26] |

ENGLE R F, SOKALSKA M E. Forecasting intraday volatility in the US equity market. Multiplicative component GARCH[J]. Journal of Financial Econometrics, 2012, 10(1): 54-83.

doi: 10.1093/jjfinec/nbr005 |

| [27] |

BOLLERSLEV T, HOOD B, HUSS J, et al. Risk everywhere: Modeling and managing volatility[J]. The Review of Financial Studies, 2018, 31(7): 2729-2773.

doi: 10.1093/rfs/hhy041 |

| [1] | 蔡毅,王晓宾,陈蕊丽,韩珣. 基于笔迹的书写者性别与年龄检测研究综述[J]. 数据与计算发展前沿, 2026, 8(1): 129-147. |

| [2] | 万萌, 何洪林, 任小丽, 聂宁明, 曹荣强, 王宗国, 李凯, 王晓光, 王彦棡, 王珏, 高超. 基于工作流的陆地生态系统碳循环实时同化预测系统[J]. 数据与计算发展前沿, 2026, 8(1): 168-182. |

| [3] | 米赛雪,张琪,张士豪,李根. 基于多模态特征的短视频热度预测研究——以抖音平台为例[J]. 数据与计算发展前沿, 2026, 8(1): 183-194. |

| [4] | 水映懿, 张琪, 李根, 张士豪, 吴尚. 基于多类特征的社交网络影响力预测研究综述[J]. 数据与计算发展前沿, 2025, 7(1): 2-18. |

| [5] | 纪鹏,牛铁,危婷,彭亮. 基于XGBoost模型的超算作业运行状态预测研究[J]. 数据与计算发展前沿, 2024, 6(6): 123-129. |

| [6] | 张斌,李晨,陆忠华. 中国股票市场风险因子研究综述[J]. 数据与计算发展前沿, 2024, 6(6): 146-159. |

| [7] | 龙春, 李丽莎, 李婧, 杨帆, 魏金侠, 付豫豪. 机器学习安全推理研究综述[J]. 数据与计算发展前沿, 2024, 6(5): 1-12. |

| [8] | 陈宇镔, 洪烨, 崔文娟, 黄敏毅, 张锦玉. 基于多维度数据驱动的商品需求量预测研究[J]. 数据与计算发展前沿, 2024, 6(5): 169-177. |

| [9] | 郭学兵, 朱小杰, 唐新斋, 杨刚, 侯艳飞, 何洪林. 基于大数据流水线系统的算法模型整合方法研究——以基于机器学习方法的LiDAR数据树木生物量反演为例[J]. 数据与计算发展前沿, 2024, 6(4): 96-105. |

| [10] | 何睿琳, 杨欣怡, 孙洪赞, 李晨. 基于图特征的组织病理学图像分析方法的最新发展情况与展望[J]. 数据与计算发展前沿, 2024, 6(2): 101-116. |

| [11] | 叶旭, 杜一, 崔文娟, 沈俊杰, 谢靖, 王露笛. 机器学习技术在眼健康领域的应用[J]. 数据与计算发展前沿, 2024, 6(2): 117-133. |

| [12] | 劳思思, 田子奇. 图卷积神经网络在晶体材料研发中的应用进展[J]. 数据与计算发展前沿, 2024, 6(1): 79-93. |

| [13] | 申志豪, 李娜, 尹世豪, 杜一, 胡良霖. 基于TPA-Transformer的机票价格预测[J]. 数据与计算发展前沿, 2023, 5(6): 115-125. |

| [14] | 危婷, 彭亮, 牛铁, 张宏海. 基于特征分析的HPC失败作业的检测和根因分析[J]. 数据与计算发展前沿, 2023, 5(6): 94-103. |

| [15] | 孙一帆, 张锐, 陶杨, 高碧柔, 秦诗涵, 安超. 本地化差分隐私综述[J]. 数据与计算发展前沿, 2023, 5(5): 74-97. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||