基于矩阵值因子算法的企业年金投资组合建模与并行求解

Modeling and Parallel Computed Enterprise Annuity Portfolio Based on Matrix-Valued Factor Algorithm

基于矩阵值因子算法的企业年金投资组合建模与并行求解 |

| 杜首燕,陆忠华 |

|

Modeling and Parallel Computed Enterprise Annuity Portfolio Based on Matrix-Valued Factor Algorithm |

| Du Shouyan,Lu Zhonghua |

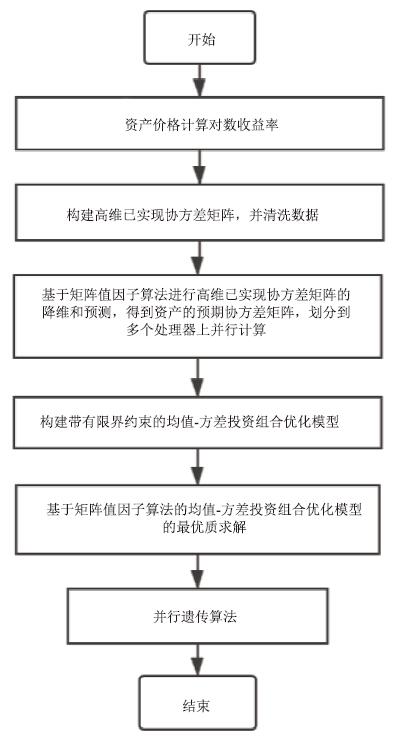

| 图1 基于矩阵值因子算法的均值-方差投资组合优化模型并行求解流程 |

| Fig.1 Parallel solution process of mean-variance portfolio optimization model based on matrix-valued factor algorithm |

|

|