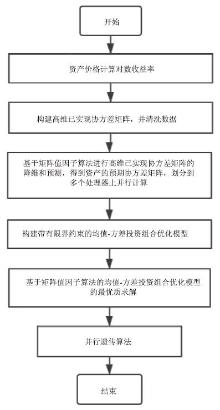

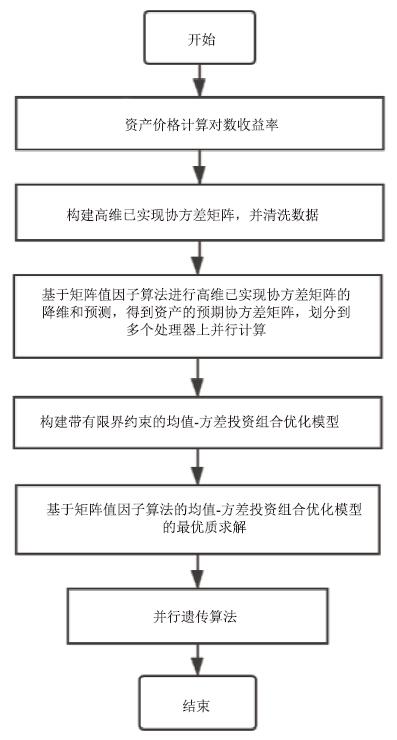

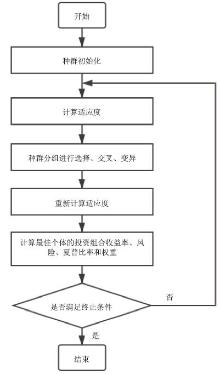

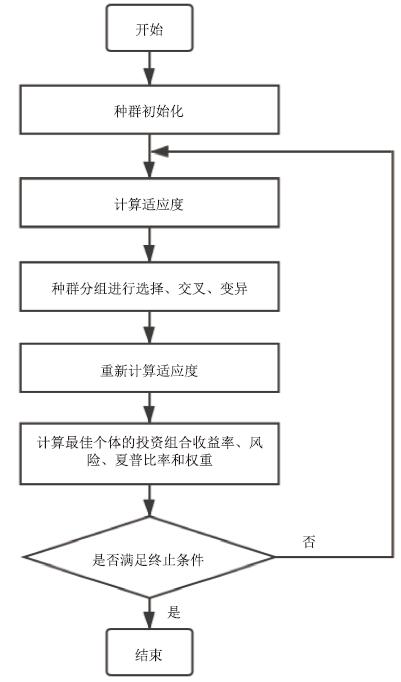

| [1] |

郭辰, 施秋圆, 郭梦云 . 优化企业年金资产配置—基于均值-CVaR模型[J]. 管理科学, 2013(9):23-27.

|

| [2] |

胡秋明, 景鹏 . 企业年金基金资产结构动态优化研究—基于DCC-GARCH-CVaR模型[J]. 保险研究, 2014(8):64-72.

|

| [3] |

余睿 . 负债驱动型企业年金投资组合最优化决策[D]. 湖南大学, 2015.

|

| [4] |

赵自强, 魏新雅 . 均衡理论下DB型企业年金资产配置最优框架设计[J]. 保险研究, 2017(2):104-114.

|

| [5] |

李洁, 彭燕, 曹晓政 . 基于投资约束条件的企业年金最优投资组合研究[J]. 金融理论与实践, 2017(7):81-84.

|

| [6] |

方中书 . 老龄化背景下企业年金基金投资运营实证分析[J]. 上海市经济管理干部学院学报, 2018,16(5):33-44.

|

| [7] |

李燕敏 . 商业银行养老金融业务发展研究[D]. 浙江工业大学, 2018.

|

| [8] |

温家琪 . 含有违约债券的企业年金最优投资问题研究[D]. 上海师范大学, 2019.

|

| [9] |

王超, 杨德平 . 基于Matlab图形用户界面的投资组合优化系统研究[J]. 青岛大学学报(工程技术版), 2019,34(2):119-125.

|

| [10] |

Feng B M, Tan Z, Zheng J . Efficient Simulation Designs for Valuation of Large Variable Annuity Portfolios[J]. North American Actuarial Journal, 2020: 1-15.

|

| [11] |

李树深 . 数据与计算是科技创新的巨大驱动力[J]. 数据与计算发展前沿, 2019,1(1):1.

|

| [12] |

张群, 张超, 黄晓霞, 应海瑶 . 基于遗传算法的风险偏好系数均值方差拓展模型[J]. 统计与决策, 2013(8):19-22.

|

| [13] |

宋鹏, 胡永宏 . 基于矩阵值因子模型的高维已实现协方差矩阵建模[J]. 统计研究, 2017,34(11):109-117.

|

| [14] |

李全亮 . 基于改进遗传算法的动态投资组合优化模型的研究[D]. 内蒙古大学, 2012.

|

| [15] |

程军 . 基于生物行为机制的粒子群算法改进及应用[D]. 华南理工大学, 2014.

|

| [16] |

戚婕 . 基于遗传算法的金融高性能计算[D]. 中南大学, 2011.

|

| [17] |

Callot L, Kock A, Medeiros M . Modeling and forecasting large realized covariance matrices and portfolio choice[J]. Journal of Applied Econometrics, 2017,32(1):140– 158.

|

| [18] |

廖方宇, 洪学海, 汪洋, 褚大伟 . 数据与计算平台是驱动当代科学研究发展的重要基础设施[J]. 数据与计算发展前沿, 2019,1(1):2-10.

|

| [19] |

李肯立, 阳王东, 陈岑, 陈建国, 丁岩 . 面向人工智能和大数据的高效能计算[J]. 数据与计算发展前沿, 2020,2(1):27-37.

|

),Lu Zhonghua1,*(

),Lu Zhonghua1,*(